The LNG Decade

North America’s Energy Dominance, the Hormuz Shock, and the Missing Link Nobody’s Trading

While investors pile into tankers and exporters, the real infrastructure bottleneck — the import terminal — sits undervalued and misunderstood. A deep dive into how the North American LNG machine works, and why Floating Storage and Regasification Units may be the cleanest trade in the sector.

Part I · The Shock

The World Just Lost a Fifth of Its LNG Supply Overnight

On March 4, 2026, Iranian forces closed the Strait of Hormuz. Within 72 hours, QatarEnergy declared force majeure on all LNG export contracts. By the end of the month, Iranian missiles had struck the Ras Laffan Industrial City complex — the world’s largest LNG processing facility — cutting Qatar’s liquefaction capacity by 17%. Energy experts now estimate repairs could take three to five years.

The numbers are staggering. Qatar supplies roughly 20% of the world’s LNG. The Strait of Hormuz routes another 20% of global seaborne LNG trade. Combined, the crisis has effectively removed close to 40% of global LNG supply from reliable delivery — creating what the head of the International Energy Agency called “the greatest global energy security challenge in history.” Asian LNG spot prices have risen over 140%. European TTF gas benchmarks nearly doubled in a month. And countries that were already running on historically low gas storage — Europe entered the crisis at just 30% capacity following a brutal winter — are now scrambling.

~20% Global LNG supply from Qatar now offline

140%+ Rise in Asian LNG spot prices since March

120 bcm IEA estimated LNG shortfall through 2030

16 Bcf/d Current US LNG export rate — a record

Into this vacuum steps the United States. America is already the world’s largest LNG exporter, having surpassed Qatar in 2023. And with the Trump administration’s aggressive “Energy Dominance” agenda — which reversed the Biden-era LNG export permit pause on Day One and has since approved ten new LNG terminal construction projects — the US is positioned as the one supplier that can actually scale. As Secretary of Energy Chris Wright told an industry conference in March: “We have a shortage of natural gas. The US is the answer.”

But here’s what most investors are getting wrong about this trade.

Everyone is buying the cargo and the ships. Nobody is buying the dock.

Part II · How It Actually Works

Anatomy of the LNG Value Chain

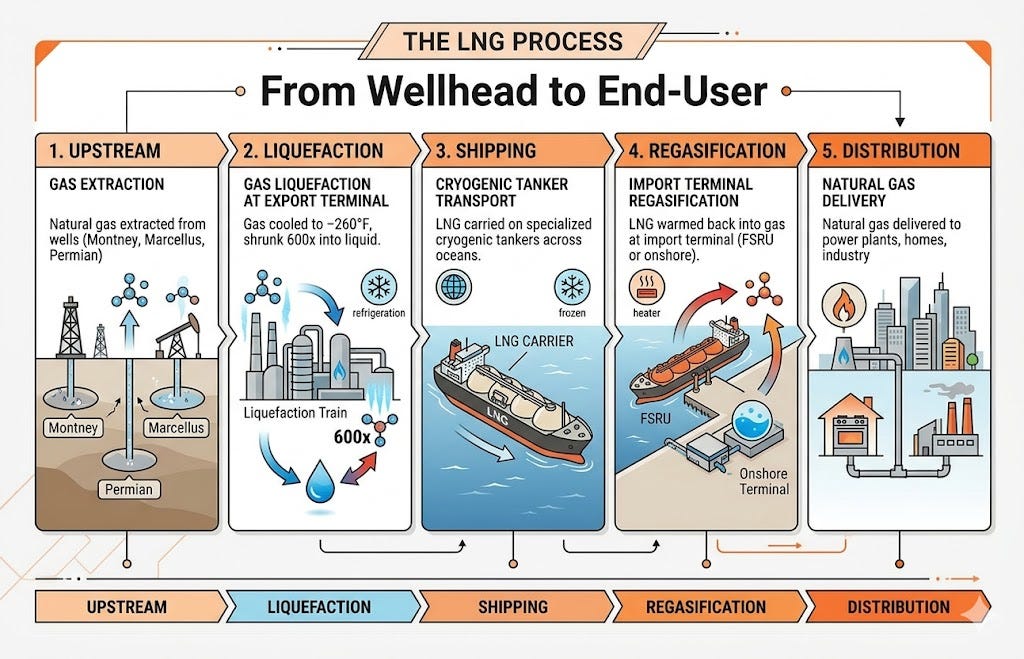

To understand where the opportunity sits, you need to understand how liquefied natural gas actually moves from wellhead to end-user. It’s a four-stage industrial process, and each stage is a distinct investment category — with dramatically different risk profiles, contract structures, and return characteristics.

The LNG Value Chain — From Wellhead to End-User

Upstream

Natural gas extracted from wells (Montney, Marcellus, Permian)

Liquefaction

Gas cooled to −260°F, shrunk 600x into liquid at export terminal

Shipping

LNG carried on specialized cryogenic tankers across oceans

Regasification

LNG warmed back into gas at import terminal (FSRU or onshore)

Distribution

Natural gas delivered to power plants, homes, industry

Stage 1: Upstream — The Gas Producers

This is where the gas comes from. In the United States, the key basins are the Marcellus/Utica shale (Appalachia), the Haynesville (Louisiana/Texas), and the Permian associated gas. In Canada, the Montney formation in northeastern British Columbia and Alberta is the crown jewel — a stacked, liquids-rich formation that will be the primary feedstock for Canada’s emerging LNG export capacity.

The upstream producers benefit from LNG export growth through a pricing mechanism: every Bcf/d of new LNG export capacity that comes online increases demand for domestic gas, which tightens the supply-demand balance and lifts gas prices at AECO (the Canadian benchmark) and Henry Hub (the US benchmark). For investors, US upstream exposure lives through companies like EQT Corporation — America’s largest gas producer, with roughly 25% of production flowing to LNG-adjacent markets. In Canada, Tourmaline Oil is the purest expression: Canada’s largest gas producer, the fifth-largest in North America, with direct stakes in the Ksi Lisims LNG project and feedstock relationships to LNG Canada.

Stage 2: Liquefaction — The Export Terminals

This is the most capital-intensive link in the chain. Converting natural gas into LNG requires cooling it to −260°F (−162°C), which shrinks it to 1/600th of its original volume, making it ship-able. A single LNG “train” — the industrial unit that performs this process — costs billions of dollars to build and takes 3–4 years from final investment decision (FID) to first cargo.

The US currently exports over 16 billion cubic feet per day through six operating export facilities, led by Cheniere Energy’s Sabine Pass and Corpus Christi terminals. The Trump administration has approved eight more projects under construction and another ten with permits but awaiting FID — with the DOE committing to expedite all future approvals as fast as possible. Goldman Sachs projects a 50% increase in global LNG supply by 2030, with the US accounting for the lion’s share.

For investors, the liquefaction stage is best expressed through Cheniere Energy (LNG) — the undisputed market leader — and the high-torque bet on Venture Global (VG), which is building aggressively but carries meaningful legal and leverage risk.

Stage 3: Shipping — The Tankers

LNG tankers are floating cryogenic vessels carrying up to 180,000 cubic meters of liquid gas. They’re expensive to build ($250M+), take 2–3 years to construct, and require highly trained crews. The market is dominated by companies like Flex LNG, Golar LNG, and GasLog.

Here’s the honest assessment of the shipping trade: it’s largely priced in. Most purpose-built LNG carriers are already committed to long-term charters. Flex LNG’s fleet is nearly 100% contracted. Golar has evolved beyond pure shipping into floating liquefaction infrastructure (FLNG) — a different and arguably more interesting business. And critically, a massive backlog of newbuild tankers ordered during the LNG boom is due to hit the water between 2026 and 2030, creating a real risk of vessel oversupply that could compress charter rates precisely as the LNG export surge hits full stride. The shipping thesis is now a yield play, not a growth play. You clip a 10% dividend from Flex LNG or you don’t.

Stage 4: Regasification — The Overlooked Bottleneck

This is where the opportunity lives — and where almost nobody is looking.

Every cargo of LNG that leaves Sabine Pass, Corpus Christi, or Plaquemines needs somewhere to go. The receiving country needs an import terminal — infrastructure that can receive a cryogenic LNG tanker, store the liquid, and convert it back into gas for injection into the local grid. Without this infrastructure, the export doesn’t happen. The cargo has no destination.

Historically, import terminals were built onshore — permanent, multi-billion-dollar facilities that take 5–7 years to permit and construct. For countries that need gas urgently (Germany after Russia’s invasion in 2022, Bangladesh right now, Iraq starting in 2026), that timeline is untenable. The solution is the Floating Storage and Regasification Unit, or FSRU — a ship-based import terminal that can be deployed in 12–18 months, repositioned between markets, and scaled rapidly to meet demand.

Part III · The Missing Link

The FSRU: Infrastructure the Market Forgot to Price

Think about the geometry of the trade. The Hormuz crisis has just permanently disrupted 20% of global LNG supply. The Trump administration is throwing regulatory fuel on the US export machine. LNG Canada and Cedar LNG are opening the Pacific corridor. Demand from South and Southeast Asia — Bangladesh, Pakistan, Vietnam, Philippines, India — is growing faster than supply. And every new molecule of LNG that needs to reach a new market needs a receiving terminal to receive it.

FSRUs are the fastest, cheapest way to build that terminal. They can be deployed in a fraction of the time and cost of onshore facilities. Germany understood this immediately in 2022 — within months of Russian gas cutoffs, Germany chartered multiple FSRUs and had import infrastructure operational by winter. That playbook is now being replicated across Asia and the Middle East as countries scramble to find alternative supply routes in the wake of the Hormuz crisis.

Everyone is buying Cheniere. Everyone is buying the tankers. Nobody is building the dock fast enough. The dock is the constraint — and it’s a public company.

The pure-play expression of this trade is Excelerate Energy (NYSE: EE) — the world’s largest and most experienced FSRU operator. And what makes EE particularly interesting is that it has evolved beyond simply leasing vessels. It now operates as an integrated LNG solutions provider — it owns the FSRU, delivers the LNG (sourcing it from QatarEnergy, Venture Global, and others), handles all terminal operations, and provides gas to the local grid under long-term contracts. It’s the full stack, from ocean to city gate, structured as a contracted infrastructure business.

What EE Looks Like on the Numbers

The financial profile is more compelling than the market currently prices:

$449M Record 2025 Adjusted EBITDA — up ~$100M YoY

$530M 2026 EBITDA guidance midpoint — +18% growth

1.6x Net debt/EBITDA — conservative for infrastructure

5x Projected EBITDA build multiple on Iraq terminal alone

The Iraq project is the near-term wildcard that most people haven’t worked through. EE is building Iraq’s first integrated LNG import terminal at the Port of Khor Al Zubair — a $520–550M project that had been on track for Q3 2026 operations. Under the minimum contracted offtake of 250 MMscf/day, the project builds at a ~5x EBITDA multiple. On a company doing $530M of EBITDA today, a project that adds ~$106M of incremental annual EBITDA — fully contracted, first-of-kind infrastructure in the world’s fourth-largest oil producer — is transformational. And the contract is scalable to 500 MMscf/day, meaning the upside case is double the base case.

Layered on top is Bangladesh — a 15-year LNG supply and regasification agreement with QatarEnergy and Petrobangla that commenced deliveries in January 2026. And behind that: a pipeline of expansion opportunities across South and Southeast Asia that management describes as the most robust organic opportunity set in the company’s history.

Part IV · The Macro Framework

Why the Timing Has Never Been Better — and May Never Be Again

Three secular forces are converging simultaneously, and they’re all pointing at the same trade.

Force 1: The Trump Energy Dominance Agenda

On Day One of his second term, President Trump signed Executive Order 14154, directing the Department of Energy to restart LNG export reviews “as expeditiously as possible” — reversing the Biden administration’s 13-month pause on new approvals. Since then, FERC has authorized ten LNG construction projects and issued 30 notices to proceed. The DOE has granted final export authorizations to terminals in Jefferson County, Texas and Cameron Parish, Louisiana. Eight projects are under construction. Another ten have permits and await FID. The regulatory tailwind is the strongest in a decade — and it’s only getting more aggressive as the Hormuz crisis validates the strategic case for US LNG supremacy.

Force 2: The Qatar Shock — A Permanent Re-rating of US Supply

The geopolitical dislocation of 2026 isn’t just a temporary price shock. Damage to Qatar’s Ras Laffan complex could take three to five years to repair. The IEA estimates a shortfall of 120 billion cubic metres of LNG between 2026 and 2030 — a number large enough to delay the previously anticipated “LNG glut” by at least two years, maintaining tight markets and elevated prices through the late 2020s. This permanently re-rates the strategic value of US and Canadian LNG supply, which cannot be choked by a regional conflict. Every European utility, every Asian industrial company, every government energy planner is now writing the same memo: we need Atlantic Basin supply, and we need the infrastructure to receive it.

The Canadian Angle: An Under-Appreciated Opportunity

While US LNG gets most of the attention, Canada is quietly building the world’s most strategically valuable LNG export corridor — the Pacific route. LNG Canada Phase 1 (Shell, Petronas, Mitsubishi, PetroChina) is ramping toward full capacity in 2026. Cedar LNG — a floating liquefaction facility near Kitimat, BC, 49.9%-owned by Pembina Pipeline and 50.1% by the Haisla Nation — is under construction targeting 2028 and has fully contracted its 1.5 MTPA of capacity to PETRONAS and Ovintiv under 12–20 year take-or-pay agreements.

The Pacific route matters because it’s the shortest shipping distance from any North American terminal to Asian markets — several days faster than Gulf Coast routes via the Panama Canal. That translates directly into lower shipping costs and higher netbacks for Pacific-routed Canadian LNG. The Canadian gas producers feeding these projects — Tourmaline (TOU), ARC Resources (ARX), and the disciplined, hedge-protected Peyto (PEY/PEYUF) — are the upstream expression of this Canadian LNG buildout.

Force 3: The Structural Deficit in Import Infrastructure

New LNG export capacity is being sanctioned at a record pace. But the receiving end of that trade — the import terminals that need to be built in Europe, South Asia, and Southeast Asia — is being built at a fraction of the necessary pace. The countries most impacted by the Hormuz closure are precisely those most dependent on FSRU-delivered LNG: Bangladesh, Pakistan, India, Vietnam, the Philippines. The IEA explicitly notes that these markets “would face production curtailments in gas-intensive industries, including fertilisers” if LNG supply remains constrained.

This is the demand signal for the FSRU market. Every country that just discovered it was 60–80% dependent on Qatari LNG for power generation is now signing emergency import terminal agreements. And FSRUs are the only technology that can be deployed fast enough to matter.

Part V · The EE Case in Depth

Excelerate Energy: The Dock Nobody Built an Investment Thesis Around

Let’s be direct about why Excelerate Energy (EE) deserves special attention in this framework — and why it’s meaningfully different from the LNG shipping names that most generalist investors lump it in with.

First: it’s not a shipping company. EE does own FSRUs, which are ships. But calling EE a shipping company is like calling a hotel company a real estate company because it owns buildings. The vessel is the delivery mechanism. The business is long-term contracted infrastructure provision in energy-scarce markets, layered with integrated LNG supply agreements. The revenue profile looks far more like a pipeline than a tanker — 15-year contracts, take-or-pay structures, government counterparties.

Second: it benefits from the LNG trade growing on both sides. More US export capacity means more cargoes. More cargoes need more receiving terminals. More receiving terminals means more FSRUs. More FSRUs means more revenue for EE. This is a pick-and-shovel play on the entire LNG export trade, not a directional bet on one side of it. EE is agnostic to whether the cargo comes from Cheniere or Venture Global — as long as it’s heading somewhere that needs receiving infrastructure, EE wins.

Third: the Hormuz crisis is an accelerant, not a one-time event. Every country in South and Southeast Asia that was dependent on Qatari LNG is now actively seeking FSRU-based import solutions. The IEA specifically calls out Bangladesh, Pakistan, and India as the most vulnerable markets — all of which are simultaneously EE’s core or target geographies. The crisis didn’t create EE’s opportunity. It compressed a five-year buildout cycle into a two-year emergency deployment cycle.

Fourth: the Iraq project is a wildcard value unlock the market hasn’t priced. A $520–550M project delivering ~$106M of incremental annual EBITDA at minimum contracted volumes — with upside to double that if offtake scales — represents a roughly 20% EBITDA step-up on a company valued at ~$2.5B market cap. Iraq is the world’s fourth-largest oil producer, a country with chronic gas deficits powering its grid on expensive oil-fired generation, and a government that has signed a minimum five-year contract with expansion options. This is not speculative — it’s a Q3 2026 operational event. A cessation to the conflict in the Persian Gulf could unlock this rerating catalyst over the next 6-18 months.

Risk Factors — Know What You’re Buying

Iraq execution risk. The capital cost has already been revised upward from $450M to $520–550M due to design changes. Any further delays or overruns would pressure near-term FCF and sentiment.

Geopolitical concentration. EE’s growth markets — Bangladesh, Pakistan, Iraq — are not known for political stability. Contract enforcement risk is real, even with government counterparties.

Interest rate sensitivity. Infrastructure businesses with 1.6x leverage are sensitive to rate movements. Rising rates increase cost of capital for growth projects.

Newbuild FSRU competition. As more operators order new FSRUs, the supply of competing vessels increases, potentially pressuring charter rates on vessels that come off contract.

EPS volatility. EE missed Q4 2025 EPS by $0.03 ($0.29 vs $0.32) despite record EBITDA — the stock dropped ~11% on the print. The market is unforgiving of misses on EPS even when underlying EBITDA is strong. Position accordingly.

Conclusion

The Trade in One Paragraph

The Hormuz crisis permanently elevated the strategic value of US and Canadian LNG supply. The Trump administration is throwing regulatory fuel on the export machine. Goldman Sachs projects an 84% increase in US LNG supply over five years. But every new molecule of LNG that gets exported still needs infrastructure on the receiving end — and that infrastructure is the constraint that nobody is talking about.

Cheniere (LNG) is the quality compounder — own it in the IRA, collect the growing dividend, watch the buyback shrink the float. Venture Global (VG) is the torque play — position sized for a potential 40% loss if BP goes wrong, but a multi-bagger if it doesn’t. EQT and Tourmaline are the upstream gas levered longs as Henry Hub and AECO tighten. Pembina and Peyto are the Canadian infrastructure and low-cost gas expressions — more defensive, still levered to the theme.

And then there’s Excelerate Energy (EE) — the company building and operating the docks that all those tankers need to pull into. A contracted infrastructure business growing EBITDA 20% annually, with a transformational Q3 2026 catalyst in Iraq and an entire generation of demand growth in South and Southeast Asia ahead of it. Trading at ~9–10x forward EBITDA with analyst consensus targets implying 26–30% upside, and a bull case from Northland at $50 that implies nearly 80% from current levels.

The LNG trade is real, it’s secular, and the geopolitics of 2026 have made it more urgent than anyone anticipated. The question is where in the value chain you want to sit. The answer that’s most underowned, most differentiated, and most directly tied to the structural growth of the entire trade — is the infrastructure that receives it.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a solicitation to buy or sell any security. All investment decisions involve risk, including the possible loss of principal. The author and publisher may hold positions in securities mentioned in this article. Past performance is not indicative of future results. All data sourced from public filings, earnings releases, IEA reports, and news sources as of April 25, 2026. Consult a qualified financial advisor before making investment decisions. Readers should conduct their own due diligence before investing in any security mentioned herein.

Hey Sue, thanks for the reply. I'm not sure on the no kings/war front. But, the whole North American based hydrocarbon system is a beneficiary of the war in Iran, yes. And you are correct: if prices stay this high, or higher long term, US based companies will be investing in building out more capacity and infrastructure. EE is the company building the fastest "Lego" piece that allows all the non-producing countries to receive and store LNG quickly. Part of the risk of the administration keeping prices lower for longer by releasing stores, is that will stop companies from investing current profits into expansion, which leads to an even worse long term shortage as the war persists

Lots to think about. So...the corruption is bigger than i realized...if I understood (sort of) this is a big win for the us based system? ...if they can get the "legos" together fast enough?

So...again if I understand...maybe we are being played with "no war" "no kings"...I keep feeling like an even smaller chess piece being used by James Bond villain...